Families often want to change old trusts for good reasons. A trust may be outdated, too rigid, tax-inefficient, difficult to administer, or poorly matched to current family circumstances.

But fixing a trust can create tax consequences if the change shifts value from one person to another. That is where gift tax risk can arise.

The issue is not simply whether the trust change is allowed under state law. A modification may be valid under the trust statute, approved by beneficiaries, or accepted by a court, but still require federal tax analysis.

Gift tax questions often arise when beneficiaries give up rights, consent to reduce their interests, allow another person to receive more benefits, or agree to make trust assets available to someone who previously had no access.

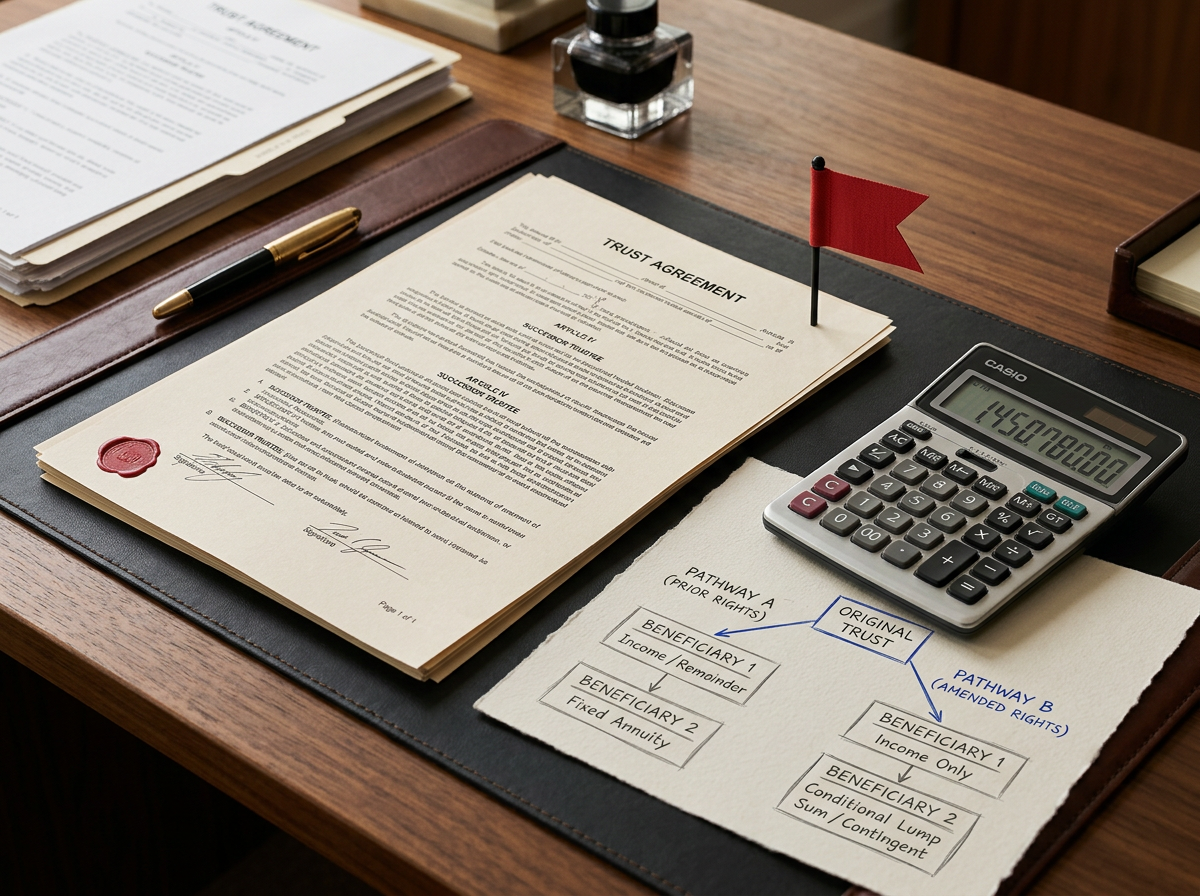

For example, suppose a trust gives one beneficiary a fixed income right and another beneficiary the remainder after that person’s death. If the beneficiaries agree to change the trust so that the current beneficiary can receive more principal, the remainder beneficiary may be giving up something of value. That may raise a gift tax question.

Similar concerns can arise when a trust is modified to add a grantor reimbursement power, expand a spouse’s access, change distribution standards, terminate a trust early, alter powers of appointment, or shift beneficial interests among family members.

The fact that everyone agrees does not automatically eliminate the issue. A beneficiary may be making a taxable transfer by consenting to a change that reduces that beneficiary’s economic interest.

This does not mean every trust modification causes gift tax. Many administrative changes do not shift economic value. Some modifications simply clarify terms, change trustee mechanics, improve administration, or address issues that do not alter beneficial interests.

The key question is whether the change affects who can benefit from the trust, when they can benefit, or how much they can receive.

Timing also matters. If a trust is changed before a taxable event, the change may define the rights going forward. If a change is made after rights have already become fixed, the tax analysis may be different. Court orders, settlement agreements, beneficiary consents, decanting, and trustee actions may all have different consequences.

Before attempting to fix a trust, families should ask:

- Whose rights are being changed?

- Is anyone giving up an economic benefit?

- Are trust assets becoming available to someone new?

- Are current and future beneficiaries affected differently?

- Does the change alter income, principal, timing, or control?

- Will a gift tax return be needed?

Trust repair can be valuable, but it should be handled carefully. The goal is to solve the old problem without creating a new tax problem.